**The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming** Why are so many people suddenly asking how to transfer credit card balances in ways that challenge everyday financial logic? What starts as a quiet curiosity rapidly spreads across mobile screens, fueled by shifting money habits and new digital tools. At first glance, transferring large card amounts seems straightforward—but the hidden twist reshapes how rewards, credit utilization, and spending limits interact in ways few realize until they try it. This pairing defies traditional banking expectations, creating powerful new opportunities for budgeters and consumers—but only if you understand the evolving mechanics behind the process. ### Why The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming Is Gaining Attention in the US In a climate of rising household expenses and complex credit ecosystems, small but impactful changes in how banks manage balance transfers are sparking broader attention. With consumers increasingly turning to multi-use financing, careful transfer planning is emerging as a strategic tool—not just a routine bank feature.

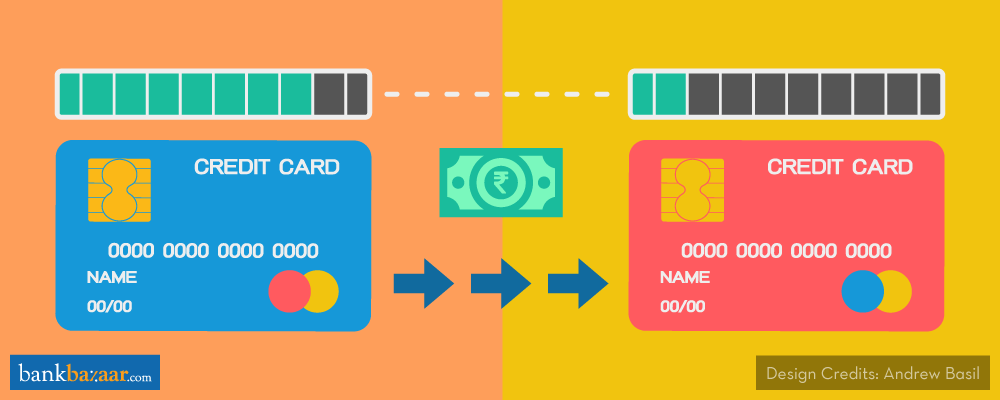

This topic surfaces repeatedly in mobile searches, social chatter, and personal finance forums—proof it’s not temporary noise, but a shift in financial awareness. ### How The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming Actually Works Transferring credit card balances isn’t simply moving a number from one card to another. The true twist lies in how banks and fintech tools now use timing, credit utilization, and reward cycles to shape outcomes you may not anticipate. When a balance transfer shifts a large amount to a new card within a short window, credit scoring models interpret this change differently—impacting available credit and perceived risk. Some issuers adjust utilization ratios by freezing or increasing limits automatically, altering your effective borrowing capacity without visible notifications. Additionally, transfers timed around billing cycles can reset interest periods, offering temporary relief from high APRs. Meanwhile, rewards points earned on the original card don’t always roll over—unless the transfer preserves active earning eligibility, a detail buried in terms but critical to long-term value. These nuances transform the transfer from a simple transaction into a strategic move, impacting cash flow, score health, and reward accruals in subtle but meaningful ways. ### Common Questions People Have About The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming **Q: Can transferring my balance actually improve my credit score?** Sometimes—particularly when the transfer refreshes your credit age or resets utilization ratios, but it depends on timing and issuer policies. Sudden shifts may trigger new credit inquiries, but thoughtful transfers can support, rather than harm, scoring over time. **Q: Does moving my balance affect my available credit?** Yes—depending on how transfers modify your credit utilization. Banks may adjust your available limit temporarily, especially if the new balance moves from used to unused segments. **Q: Are there transfer methods with hidden costs or penalties?** While many digital tools offer fee-free transfers, some promotional plans behind the scenes limit reward transferability or reset points on closed cycles. Always review terms before transferring, especially during short-term flash offers. **Q: How does timing impact my returns?** Transfers aligned with billing cycles or rebate periods maximize value. For example, rolling over into a card offering new sign-up bonuses during a seamless transfer window enhances total benefits without added friction. ### Opportunities and Considerations The twist behind these transfers offers real upside: smarter balance management, better reward capture, and proactive credit tracking. For budgeters, it opens a path to minimize interest while maximizing liquidity. Yet risks remain: missed cutoff dates, unexpected credit line drops, or reward truncation. Users must balance convenience with due diligence—especially with rolling multi-card strategies. This isn’t a get-rich-quick solution, but a refined tactic in modern finance that rewards informed, mindful use.

**Q: How does timing impact my returns?** Transfers aligned with billing cycles or rebate periods maximize value. For example, rolling over into a card offering new sign-up bonuses during a seamless transfer window enhances total benefits without added friction. ### Opportunities and Considerations The twist behind these transfers offers real upside: smarter balance management, better reward capture, and proactive credit tracking. For budgeters, it opens a path to minimize interest while maximizing liquidity. Yet risks remain: missed cutoff dates, unexpected credit line drops, or reward truncation. Users must balance convenience with due diligence—especially with rolling multi-card strategies. This isn’t a get-rich-quick solution, but a refined tactic in modern finance that rewards informed, mindful use. ### What The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming May Be Relevant For This insight applies across diverse financial situations—whether you’re a student managing first credit, a parent optimizing household spending, or a savvy user leveraging rewards. It matters if you pay interest monthly or hope for promotional bonus cash. Even small changes in transfer timing can influence your credit footprint in ways you’d never envision, making awareness critical. Whether simplifying debt, accentuating benefits, or avoiding pitfalls, understanding this twist empowers smarter decimal-by-decimal decisions. ### Things People Often Misunderstand Myth: Transferring a balance never changes your credit utilization. Reality: The transfer can reset your utilization ratio temporarily, especially when moving large amounts into underused credit segments. Myth: All balance transfer services treat rewards the same. Reality—some preserve eligibility or cap point expiration; others eliminate points entirely post-transfer. Myth: Transfers are Always Interest-Free. Reality: Many promotions delay APR rates for 12–18 months, but interest still accrues after the grace window, often at standard or higher rates. Understanding these nuances builds realistic expectations and prevents costly surprises. ### Soft CTA Stay ahead in a dynamic financial landscape by mastering the subtle mechanics behind your credit card transfers. Explore how timing, scoring signals, and reward structures work together—tools that can quietly improve your financial health without demanding extra effort. Curious to refine your own strategy? A quick review of your credit bureau reports and issuer terms can reveal untapped potential—start small, stay informed. ### Conclusion The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming isn’t just a financial footnote—it’s a quiet shift redefining how consumers manage debt, rewards, and credit together. For US users navigating rising costs and complex tools, understanding this twist builds smarter habits. It’s not about mastering every detail overnight, but about recognizing how seemingly routine moves shape long-term outcomes. Stay curious, stay informed, and let knowledge guide your next dollar movement—because even a small financial insight can spark meaningful change.

### What The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming May Be Relevant For This insight applies across diverse financial situations—whether you’re a student managing first credit, a parent optimizing household spending, or a savvy user leveraging rewards. It matters if you pay interest monthly or hope for promotional bonus cash. Even small changes in transfer timing can influence your credit footprint in ways you’d never envision, making awareness critical. Whether simplifying debt, accentuating benefits, or avoiding pitfalls, understanding this twist empowers smarter decimal-by-decimal decisions. ### Things People Often Misunderstand Myth: Transferring a balance never changes your credit utilization. Reality: The transfer can reset your utilization ratio temporarily, especially when moving large amounts into underused credit segments. Myth: All balance transfer services treat rewards the same. Reality—some preserve eligibility or cap point expiration; others eliminate points entirely post-transfer. Myth: Transfers are Always Interest-Free. Reality: Many promotions delay APR rates for 12–18 months, but interest still accrues after the grace window, often at standard or higher rates. Understanding these nuances builds realistic expectations and prevents costly surprises. ### Soft CTA Stay ahead in a dynamic financial landscape by mastering the subtle mechanics behind your credit card transfers. Explore how timing, scoring signals, and reward structures work together—tools that can quietly improve your financial health without demanding extra effort. Curious to refine your own strategy? A quick review of your credit bureau reports and issuer terms can reveal untapped potential—start small, stay informed. ### Conclusion The Surprising Twist Behind Transferring Credit Card Amounts You Never Saw Coming isn’t just a financial footnote—it’s a quiet shift redefining how consumers manage debt, rewards, and credit together. For US users navigating rising costs and complex tools, understanding this twist builds smarter habits. It’s not about mastering every detail overnight, but about recognizing how seemingly routine moves shape long-term outcomes. Stay curious, stay informed, and let knowledge guide your next dollar movement—because even a small financial insight can spark meaningful change.

Stop Wasting Time—Zoho Books Has the Secret

You Won’t Believe What This YouTube Downloader Gets You

Shocking Discovery on Kahoot It Changes How Everyone Play Kahoot Forever